For a deeper look into our DataScope Select SOAP API, look into:

Overview | Quickstart | Documentation | Downloads | Tutorials

1

●0 ●1 ●0

How to extract all LIBOR rates(USD, GBP, CHF, EUR, JPY) with all 7 different maturities(Overnight, 1 week, 1 month, 2 month, 3 month, 6 month, 12 month) by sending request to DSS REST API? Please give an example, urgent.

11.3k

●25 ●8 ●13

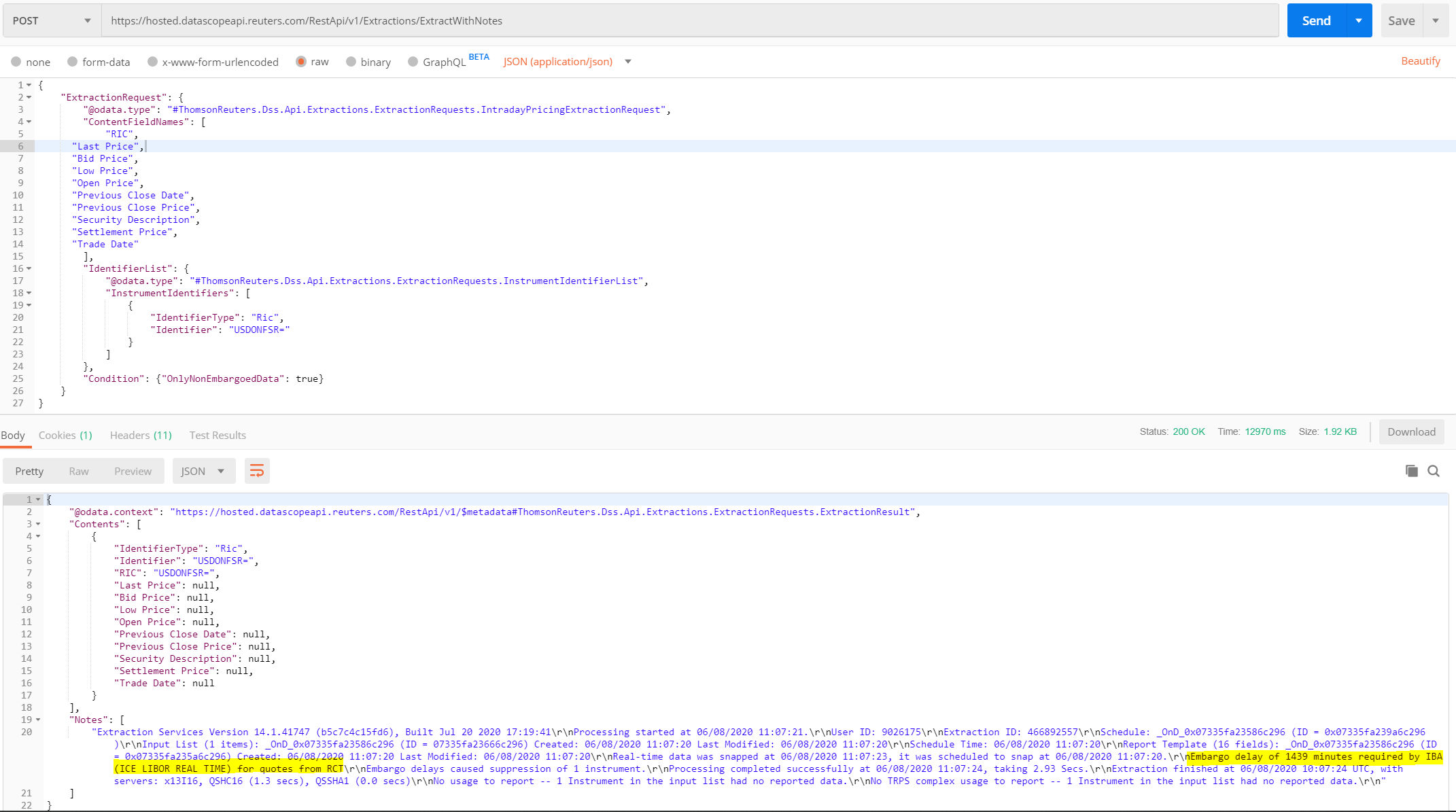

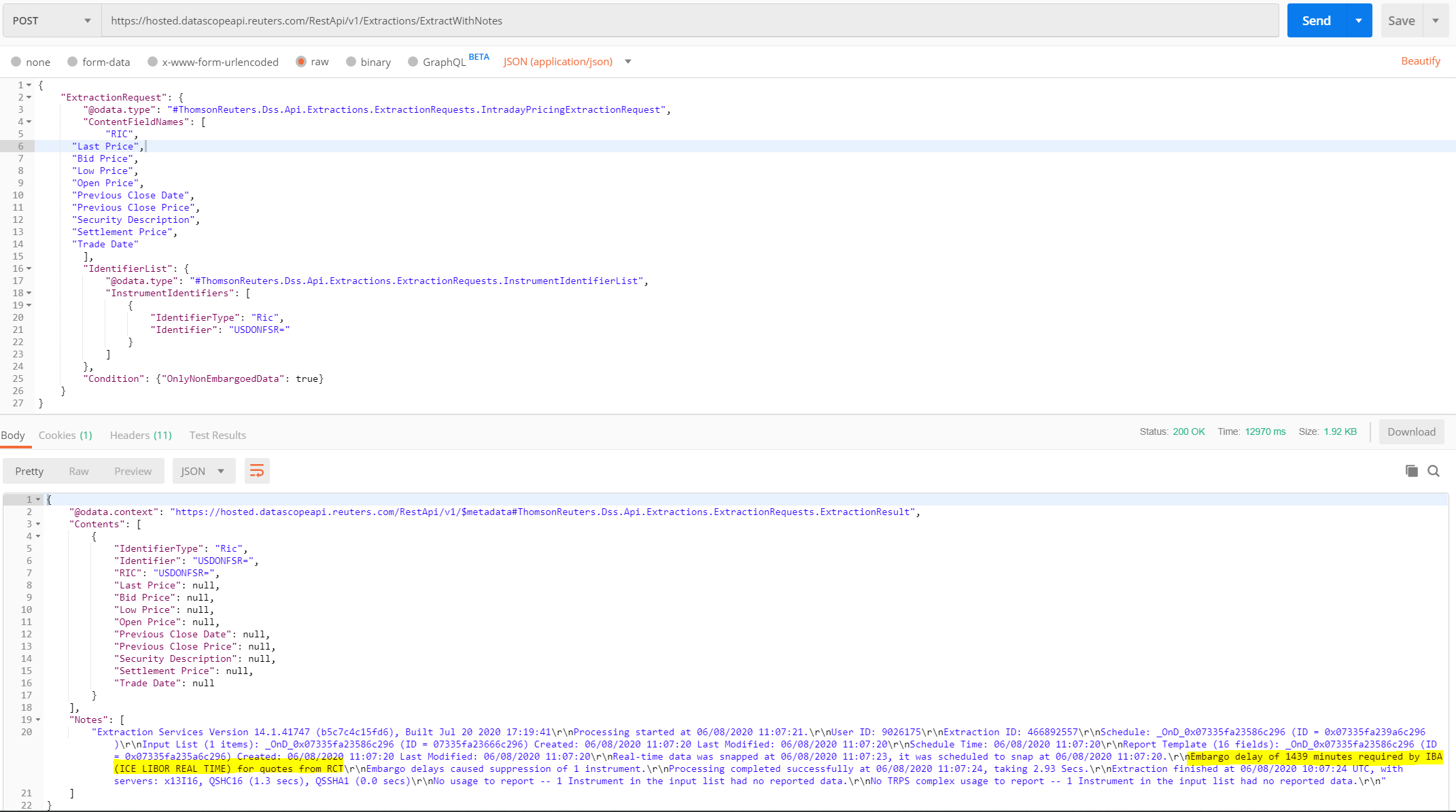

The rates and maturities could be identified using RIC name. For example, USD overnight rate, the RIC should be on USDONFSR=. If the extraction takes tool long to complete, it possibly is due to embargo. Please find more information in this tutorial.

Anyway, you can try the /LIBOR=which is delayed RIC. The delayed RIC is not affected by embargo.

Below is the request sample.

{

"ExtractionRequest": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.IntradayPricingExtractionRequest",

"ContentFieldNames": [

"RIC",

"Last Price",

"Trade Date"

],

"IdentifierList": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.InstrumentIdentifierList",

"InstrumentIdentifiers": [

{

"IdentifierType": "ChainRIC",

"Identifier": "/LIBOR="

}

]

}

}

}

all fields are null...

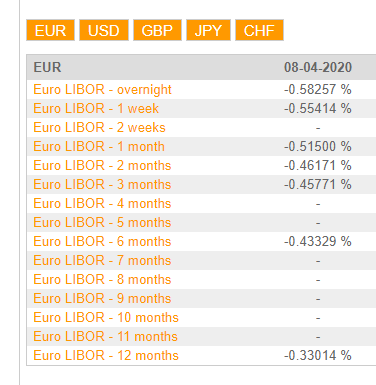

These are LIBOR rates I queried from other websites. So what the request template should be if I want to retrieve today or yesterday LIBOR rates (in 7 maturities (from overnight to 12 months) and in 5 different currencies mentioned in the question) ?

@beatgtech,

As you can see, the Notes fields indicates that the extraction was embargoed because your account doesn't have permission for ICE LIBOR Real-time. You will get the extracted data after 1439 minutes. Please contact your Refinitiv account manager for the permission issue.

Anyway, you can try the /LIBOR= RIC instead for previous day data.

11.3k

●25 ●8 ●13

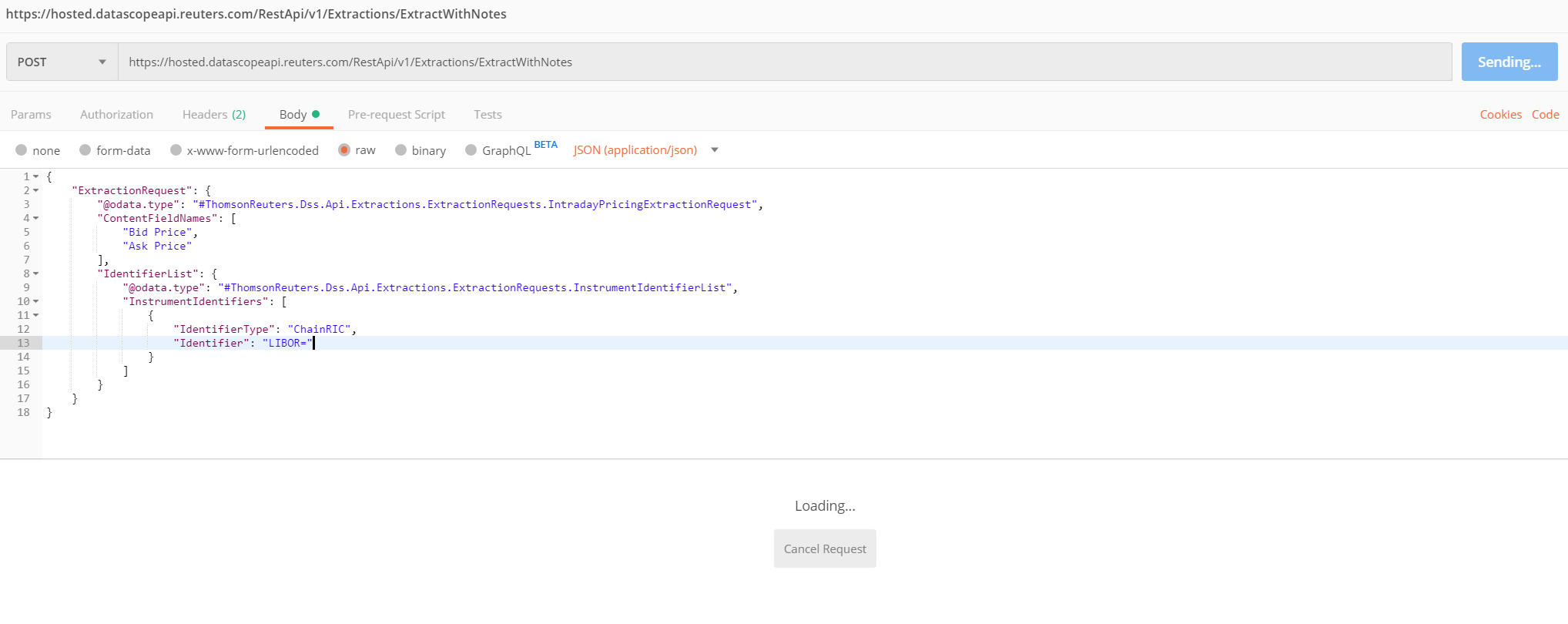

Hi @beatgtech,

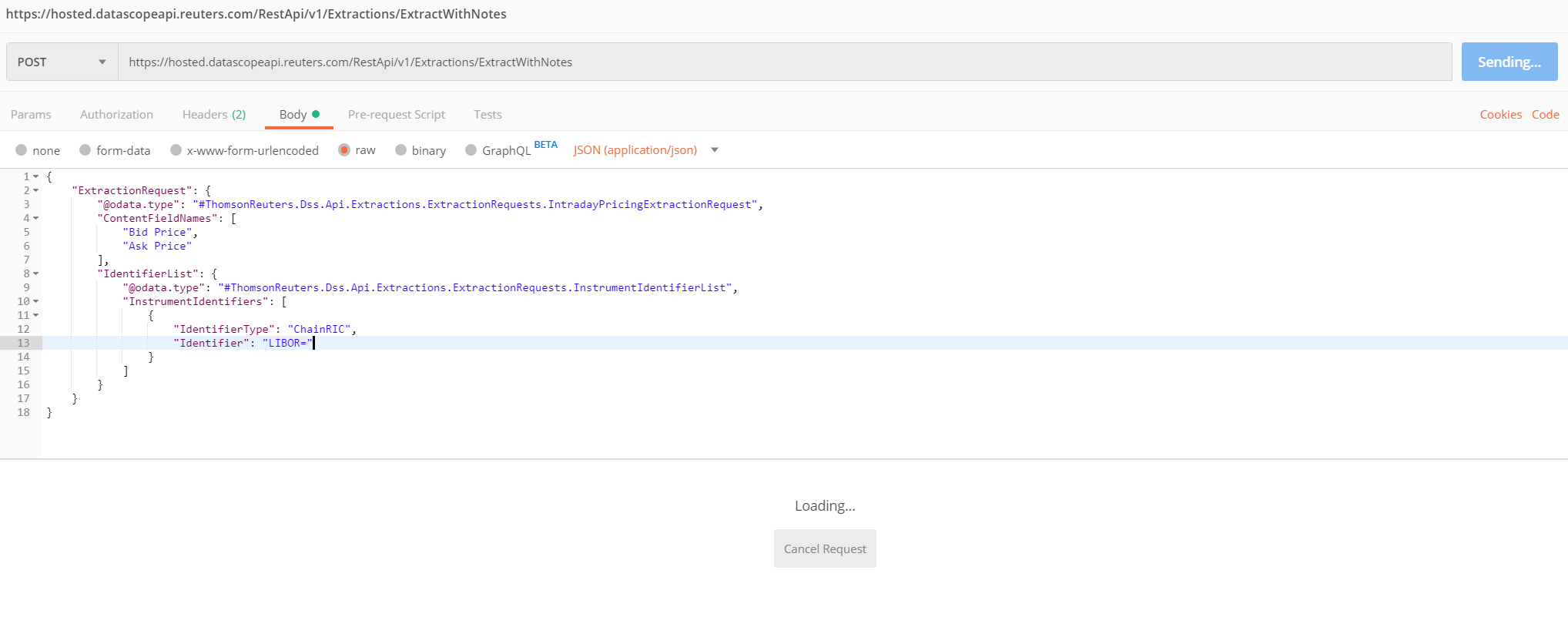

You can use chain RIC: LIBOR= to extract all LIBOR rates. Below is the sample of request.

{

"ExtractionRequest": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.IntradayPricingExtractionRequest",

"ContentFieldNames": [

"Bid Price",

"Ask Price"

],

"IdentifierList": {

"@odata.type": "#ThomsonReuters.Dss.Api.Extractions.ExtractionRequests.InstrumentIdentifierList",

"InstrumentIdentifiers": [

{

"IdentifierType": "ChainRIC",

"Identifier": "LIBOR="

}

]

}

}

}

{kind=link}

{kind=link}

{kind=link}