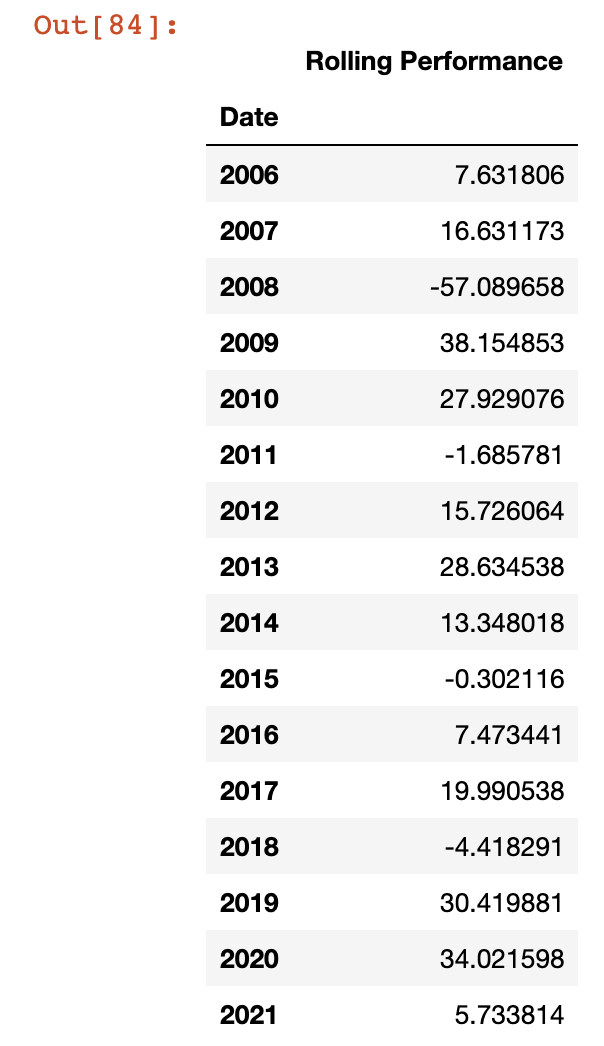

I can use the field TR.FundRollingPerformance to get fund returns since inception, by year etc.

However, if I used the parameters: TR.FundRollingPerformance(RollTimeFrame=10Y Interval=Y)

The result I get are 1-year periods, ending at month-end of the previous month.

(I.e. if I pull the data in June, I get a series of yearly values, for years ending May 31st.

I am trying to get the annual results for calendar years. Are there any parameters that can be used with this field in order to get this?

Given how the data will ultimately be used, the idea solution would be single formula returning a single value (for a year). Something like:

TR.FundRollingPerformance(RollTimeFrame=2018 Interval=Y)

Is there any way to do this? The only working solution I have seen is to pull a table of the monthly returns, then sum all of them for a specific year. That approach won't work in this case.