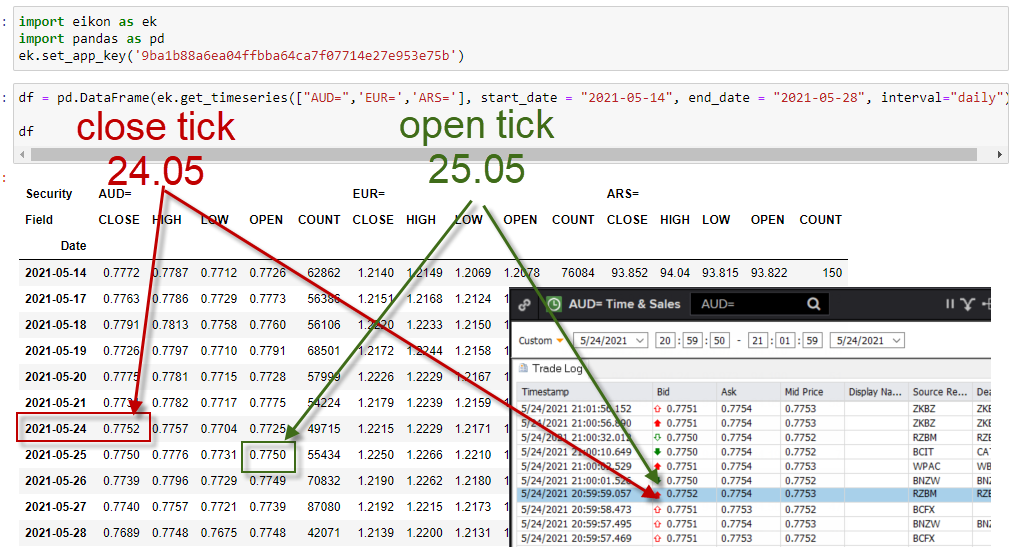

I would like to know

A) at what time historical timeseries for fx data roll over when I run a python request. What is the default timezone and time of the historic data rollover for fx data?

B) can I request in python a specific timezone or time when requesting historical daily fx data? For example I want the daily close to be EST 5pm or UTC midnight for historical fx time series requests. Bloomberg offers that with parameter overrides. How can I do this with the python api via Eikon?