I am working on adjusting the prices for dividends and therefore need to calculate total return index for every given day. This is the function is wrote:

def get_ts_for_ric(ric):

ric_tr = ek.get_data(ric, ["TR.TotalReturn.date","TR.TotalReturn.value"], parameters={"Frq": "D", "SDate": "2011-01-01", "EDate": "2020-12-31"})[0].set_index("Date").sort_index()

for i in range(ric_tr.shape[0]):

if i == 0:

ric_tr.loc[ric_tr.index[i], 'tri'] = 1 + ric_tr['value'][i]/100

else:

ric_tr.loc[ric_tr.index[i], 'tri'] = ric_tr['tri'][i-1] * (1 + ric_tr['value'][i]/100)

ric_close = ek.get_data(ric, ['TR.ClosePrice.Date', 'TR.ClosePrice.Value'], parameters={"Frq": "D", "SDate": "2011-01-01", "EDate": "2020-12-31"})[0].set_index("Date").sort_index().dropna()

ric_ts = ric_tr.join(ric_close['Close Price'], how='inner')

cp_to_tri = ric_ts['Close Price'][-1]/ric_ts['tri'][-1]

ric_ts['adjusted'] = ric_ts['tri'] * cp_to_tri

return ric_ts

When I use it for a RIC, for example:

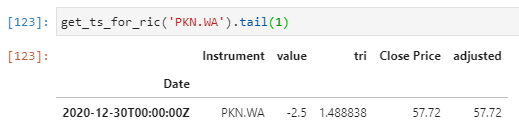

get_ts_for_ric('PKN.WA')

I get the following last row as a result:

So that the total return index ('tri' column) indicates a Total Return for the period of 48,88%.

However when I try to get from the API the Total Return for this period directly:

ek.get_data('PKN.WA',['TR.TotalReturn'],{'SDate':'2011-01-01', 'EDate':'2020-12-31'})[0]

I get this:

So over 10 percentage points more than calculated from daily total returns.