I'd like to get with one call a time-series of intraday numbers for "Quotes" , "volume" , and "vwap" ? I tried the new python Data Platform which does the job for quotes but 'volume' and 'vwap' are missing. One minute time Interval if possible.

For a deeper look into our Eikon Data API, look into:

Overview | Quickstart | Documentation | Downloads | Tutorials | Articles

12

●1 ●2 ●5

Is it possible to get in one call, a time-series of intraday numbers for "Quotes" , "volume" , and "vwap" ?

6.7k

●8 ●6 ●7

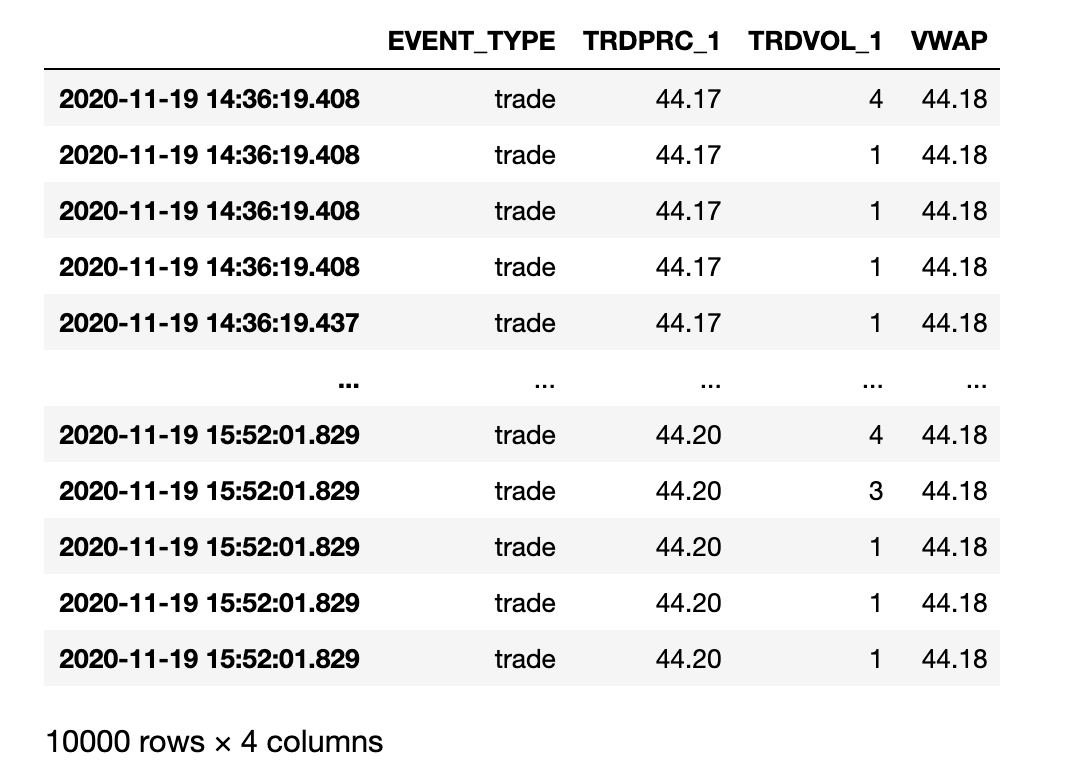

@davide.costanzo This call to the historical pricing events can get you trade and quote level details you want. This call does not provide time-aggregated summaries. You would need to do this yourself.

df1 = rdp.get_historical_price_events(universe = 'LCOF1', eventTypes = ['trade','quote'], fields = ['TRDPRC_1','TRDVOL_1','VWAP']) display(df1)

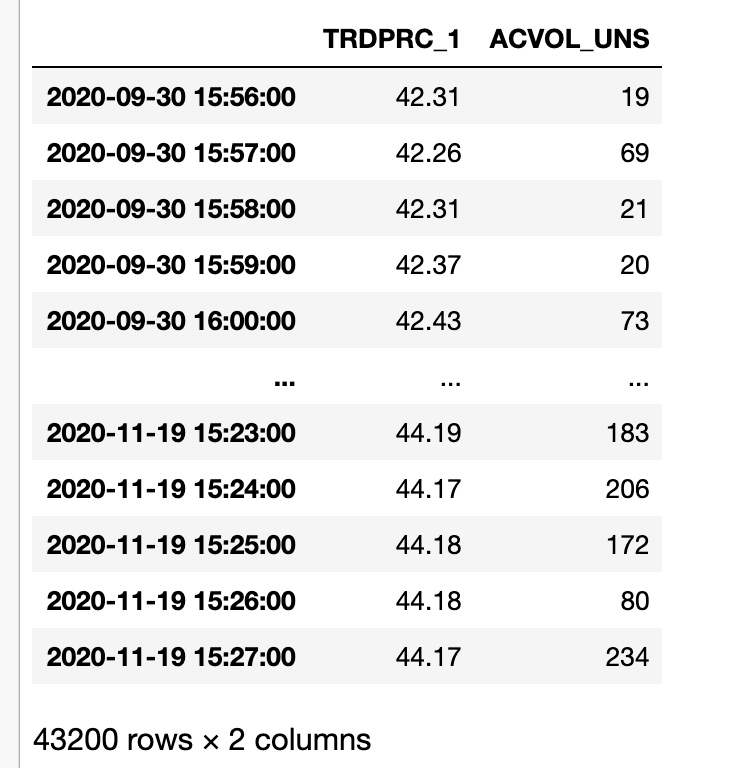

The historical pricing summaries function provide one minute aggregation but no VWAP.

df1 = rdp.get_historical_price_summaries(universe = 'LCOF1', interval = rdp.Intervals.ONE_MINUTE, fields = ['TRDPRC_1','ACVOL_UNS']) display(df1)

Is this the kind of thing you were after?

6.7k

●8 ●6 ●7

@davide.costanzo do you mean you are using the get_timeseries api call - which does provide OHLC and volume at 1 min resolution?

Or are you referring to the Refinitiv Data Platform Historical Pricing API ? Please could you provide the API call you are using.

12

●1 ●2 ●5

thanks for answering. The get_timeseries (of the Eikon API) gives indeed OHLCV candles , while the rdp.get_historical_price_summaries() (of the Eikon Data Platform) provides the QUOTES. I am wondering if it is possible to get the VOLUME and the QUOTES in one call at the same time (and the VWAP possibly), for 1 minute time interval.

6.7k

●8 ●6 ●7

@davide.costanzo can you give me an example RIC and I will try to get you the correct API call. For example if its an FX RIC you could use the Count field of the get_timeseries for an indication of volume. VWAP would only come from Historical Pricing Events function - which you may need to aggregate to 1 min horizon. Send me a sample RIC and I will try.