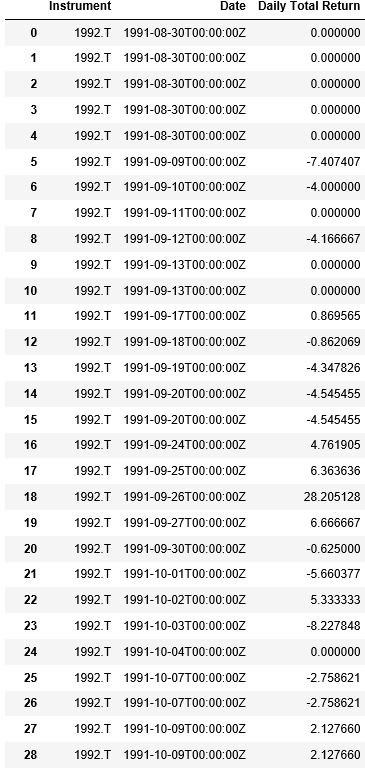

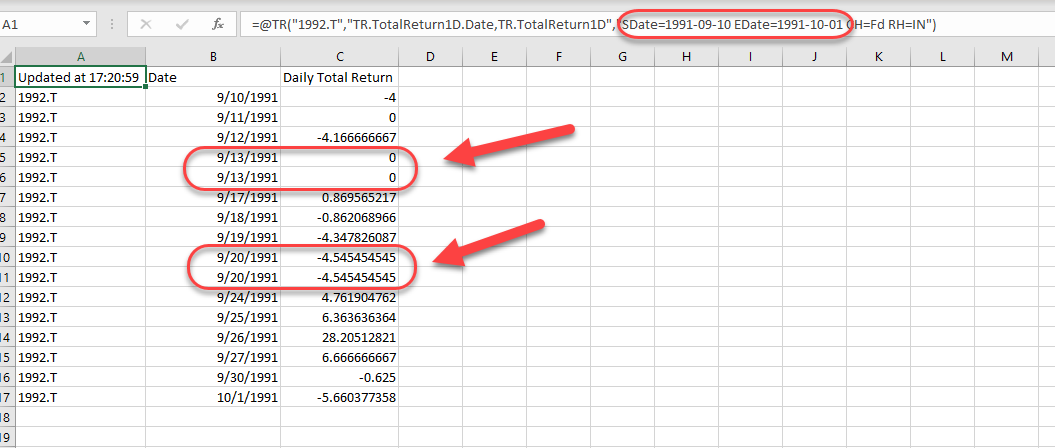

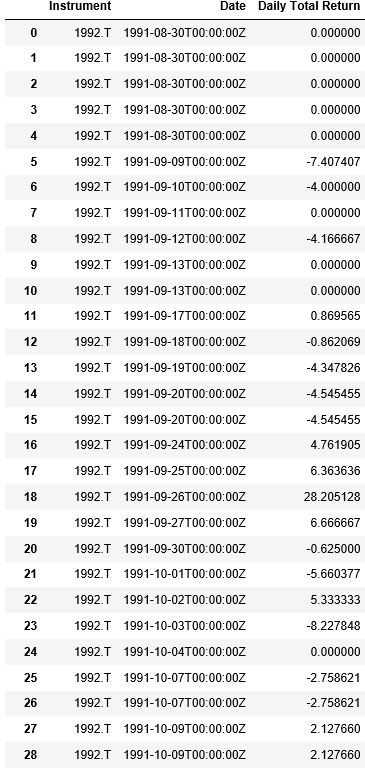

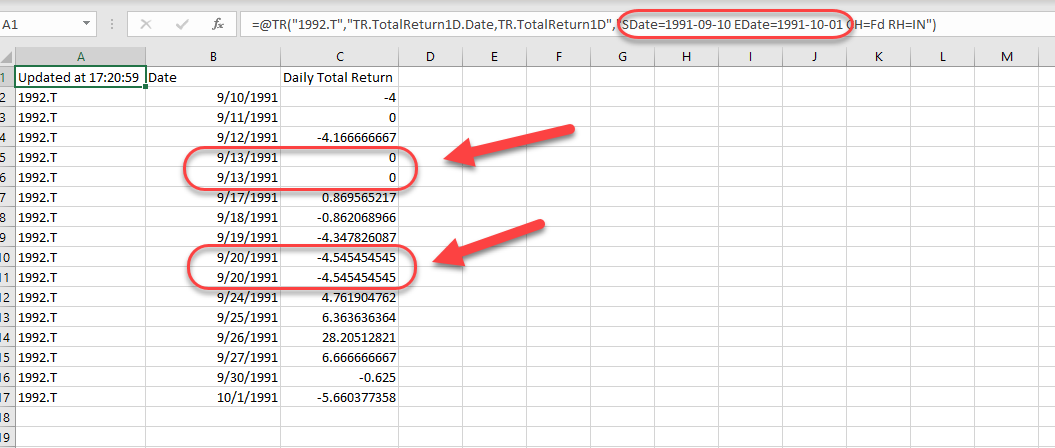

Hi, my question is about what is an efficiency way of doing this:

Let's say I have a particular date of interest for a RIC, and I want to get 1) the daily total returns for -1 to 1 days around this date and 2) the total return from this date to 30 days after this date.

For now I am retrieving every return data separately by

#for the daily return from -1 to 0

=eikon.get_data([RIC,['TR.TotalReturn'], {'SDate':datetime.strftime(Date - timedelta(1), '%Y-%m-%d'), 'EDate':datetime.strftime(Date - timedelta(0), '%Y-%m-%d')})

This appears very inefficient when I have many of such dates of interest from many RICs, not to mention the Error 400 warnings. Just wonder if anyone have a clever way?

{kind=link}

{kind=link}